Evergreen Funds and the Remaking of the Venture Capital Asset

The future of venture funds is Evergreen. Coupled with the venture studio business model, a new paradigm awaits

Between 2015 and 2023, the Venture Capital (VC) industry deployed over $1.8T. By the start of 2024, more than one-third of this investing activity had evaporated in unprecedented portfolio markdowns.

As a consequence, hold times are lengthening, which drives down IRRs. This, in turn, grinds dealmaking to a halt. At the time of this publication, new fundraising, especially by new managers, is dead or dying.

We are witnessing the most extraordinary cyclical collapse in the history of venture capital investing.

Traditional VC models, characterized by their fixed-term, closed-ended fund structures, are outdated and inefficient. The high failure rates and cyclical nature of venture capital bubbles caused by the unicorn investing thesis that underpins the practice of fund stacking and fee raking have cracked open the door of potential disruptive innovation.

If the practice of venture building studios represents the future process for deciding what and when to invest, the Evergreen fund structure could be the future venture fund model, breaking the cycle of catastrophic market bubbles by offering a more resilient, long-term investment strategy.

With an indefinite lifespan and continuous reinvestment capabilities, Evergreen funds, combined with venture studios' hands-on, nurturing approach, could revolutionize the VC landscape, providing stability and sustained growth in an industry historically plagued by volatility.

Prelude to Creative Destruction: The Kaufman Institute Foreshadowing

In 2012, following a decade of recovery from the dot com collapse and feeling the fresh effects of the massive real estate crisis, the Kauffman Foundation published a scathing report about the VC industry and Kauffman’s own experience as a Limited Partner (LP).

“The most significant misalignment occurs,” they concluded, “because LPs don’t pay VCs to do what they say they will—generate returns that exceed the public market.”

As you can imagine, the Kauffman Report led to a massive overhaul of the entire VC industry and business model.

Just kidding. Nothing changed. It only got worse.

The Kauffman authors called into question the genuine motivations of VC fund managers. They pointed directly at the elephant in the room: A standard format of charging a management fee of 2% of assets plus 20% of ‘the carry’ (profits). “Under the existing 2 and 20 structure, many institutional investors pay GPs well to build funds, not build companies,” the authors conclude.

Simply put, if you follow the money, this model only incentivizes the creation of bigger funds. With bigger funds comes a bigger collapse. And the cycle repeats.

The past teaches us that value "on the books" differs from value in the bank. Yet, here we are, over twenty years after the dot-com bubble, seemingly doing more of the same thing, only bigger.

What is an Evergreen Fund and How Does It Work?

An Evergreen fund is a type of investment fund structured to have an indefinite lifespan, allowing for continuous investment and reinvestment in portfolio companies. This contrasts with traditional closed-ended funds, which have a fixed term.

Evergreen funds allow investors to enter or exit the fund at periodic intervals based on the fund's current net asset value (NAV). This flexibility is a crucial differentiator from closed-ended funds, which typically only allow new investments or withdrawals once the fund is liquidated or reaches its term-end.

In an Evergreen fund, returns generated from the fund's investments can be reinvested into new opportunities, creating a self-sustaining cycle. This reinvestment can include capital returned from successful exits, dividends, or interest income.

Not unlike other investment funds, Evergreen fund managers usually charge management fees and may also charge performance fees based on the returns generated for investors.

Structure of Evergreen Funds and How They Are Different

The open-ended structure allows for an ongoing capital raising and investment period instead of closed-ended funds, which raise a fixed amount of capital at inception and then close to new contributions.

Evergreen funds may have terms that specify the conditions for investments and redemptions, including notice periods, minimum investment periods, and fees associated with early withdrawal to ensure the fund's stability and long-term focus.

Regular valuation of the fund’s assets is critical to accurately calculating the NAV, which determines the price at which new investors can invest and existing investors can exit. Evergreen funds provide periodic liquidity opportunities to investors, contrasting with the more illiquid nature of closed-ended funds, where investors are typically committed until the end of the fund's term or until secondary market opportunities arise.

Why Evergreen Funds Make Sense Now

A more flexible, long-term investment horizon, which Evergreen funds would facilitate as we face the challenge of underwriting important industries like deep technology, where companies may take longer to mature and generate returns.

The Evergreen model's potential for closer alignment with portfolio companies' goals and timelines is another area that exposes significant advantages. This alignment can lead to better decision-making and support for companies, leading to higher success rates.

In addition, the impact of market conditions on fund performance is worthy of mention. Evergreen funds have an advantage in down markets, as they can invest or withhold capital without the pressure of a closing investment period. This flexibility can lead to better timing in investments and exits, enhancing overall performance.

Sutter Hill Ventures: The Evergreen OG

Evergreen fund structures are nothing new. Sutter Hill Ventures (SHV), established in 1962 in Palo Alto, California, is one of Silicon Valley's earliest and most influential venture capital firms. However, SHV also played a pioneering role in the adoption of the Evergreen fund model.

SHV was founded when venture capital was still in its infancy. The firm's founders, Paul Wythes and William Draper III, were among the first to recognize the potential of providing seed money to nascent technology companies in the region. From its inception, Sutter Hill Ventures established itself in Palo Alto, positioning the firm at the heart of what would become Silicon Valley's booming tech industry.

SHV stands out for creating substantial value within the Evergreen investing framework. Since 2009, SHV has been a cornerstone for major successes like Snowflake, Sigma Computing, and Lacework, contributing to nearly $100 billion in market cap. The firm shifted noticeably towards a radically different strategy in 2008, led by Mike Speiser, focusing on fewer, larger bets and directly engaging in the venture-building process.

SHV differentiates itself with a hands-on approach that has led to the founding of 20 companies out of approximately 80 in their portfolio since 2009. SHV's strategy emphasizes making fewer but more focused investments, contrasting sharply with the broader industry trend of making numerous smaller bets.

The recipe for SHV’s success includes identifying prominent macroeconomic trends and investing in solutions that solve what they can quantify as the most significant problems or challenges industries will face. SHV's venture-building process involves recruiting experts, adhering to a "40% model" for product readiness before scaling, staying agile in the early stages, and rapidly accelerating growth.

SHV is not alone. Sequoia, a Power Law Cartel stalwart, recently transitioned to an Evergreen model with the creation of the Sequoia Fund. This open-ended fund does not have a defined term for liquidating holdings and instead continuously reinvests proceeds from its investments. The Sequoia Fund allocates capital to a series of closed-end sub-funds for venture investments at every stage, from inception to IPO.

Lesser-known funds are also following suit. Thomvest Ventures operates a similar model not tied to any specific timeline. Kiko Ventures is applying the Evergreen strategy to cleantech and climate tech investments. AENU runs an Evergreen program to tackle significant environmental and social outcomes. The same goes for BioAdvance, which works closely with entrepreneurs focused on improving human health.

So Why Aren’t Evergreen Funds More Prevalent Yet?

I contend that we don’t see more Evergreen funds because the methodology is antithetical to the interests of the Power Law Cartel itself. The Cartel runs deeper than the firms that control it. It extends to the critical support ecosystem in the venture industry, including fund attorneys, fund accountants, fund administrators, and back-office fund platform providers.

Over a two-year span, I surveyed a broad cross-section of the fund support ecosystem. I was surprised at the level of openly dissuasive arguments I received.

Lawyers and accountants told me managing an Evergreen fund would be too complex, especially in handling continuous capital inflows and outflows, recalculating NAV, and dealing with the administrative aspects of allowing periodic investor exits and entries. The dynamics of exits and distributions, I was told, are too complex in an Evergreen fund, as profits from investments need to be balanced between reinvestment in the fund and distributions to investors seeking liquidity.

So-called experts said investors prefer the closed-ended structure due to its definitive timeline and the traditional harvest period toward the end of the fund’s life, aligning with their investment horizons and liquidity needs.

Even established industry veterans went to great lengths to tell me the open-ended nature of Evergreen funds would make it too challenging to measure performance against traditional benchmarks, which often rely on the precise start and end points of closed-ended funds to calculate returns.

Investment Bankers, the coin-operated capital raisers of the supply chain, said Evergreen funds require a continuous commitment to finding and investing in new opportunities, which can be more intensive than managing a finite pool of capital over a fixed term.

That same group, who benefits handsomely from selling private companies, ruled out the notion of Evergreen funds because regulatory requirements and market expectations favor the more traditional closed-ended structure. For example, they said, the closed-ended format is well-understood and has a long history of regulatory compliance and investor protection mechanisms.

Breaking the Cycle of Venture Capital Bubbles with Evergreen Funds and Venture Studios

Evergreen fund structures alone are an interesting alternative. However, integrating or combining Evergreen funds with the venture studio model presents a compelling solution to the cyclical nature of venture capital bubbles.

With their indefinite lifespan, Evergreen funds align well with the venture studio model's long-term, hands-on approach. This combination allows for a sustainable and stable investment environment, reducing the pressure to achieve quick exits and fostering a focus on building resilient companies.

The continuous reinvestment feature of Evergreen funds ensures that capital is deployed based on strategic, long-term considerations rather than short-term market trends. This approach mitigates the risk of bubbles by avoiding the herd mentality often seen in traditional venture capital, where firms rush to invest in hot sectors without thorough due diligence.

Investors can closely align with portfolio companies' growth trajectories by pairing Evergreen funds with venture studios. Venture studios' deep involvement in daily operations and strategic decision-making, coupled with the financial flexibility of Evergreen funds, supports the sustained development of startups. This model aligns investment horizons with the timeframes needed for companies to mature, reducing the likelihood of premature exits driven by fund lifecycle constraints.

The flexibility inherent in Evergreen funds allows for strategic timing in investments and exits, enhancing overall portfolio performance. Venture studios share risk better than any other venture-building model. This allows them to better and more strategically navigate market downturns, thereby optimizing returns for investors. This strategic timing ability, coupled with no undue pressure to deploy capital in search of foolish Unicorns, avoids a common pitfall in traditional VC models.

A Glimpse of the Future? A Review of the OSS Ventures Model

Earlier this year, I attended a presentation from the founder of OSS Ventures. OSS is an innovative venture studio and fund whose approach has created over 15 startups within four years, deploying their solutions in more than 1080 European factories. Their success is worth paying attention to as a master class executing the venture studio playbook.

But something else about what they are doing that stood out to me.

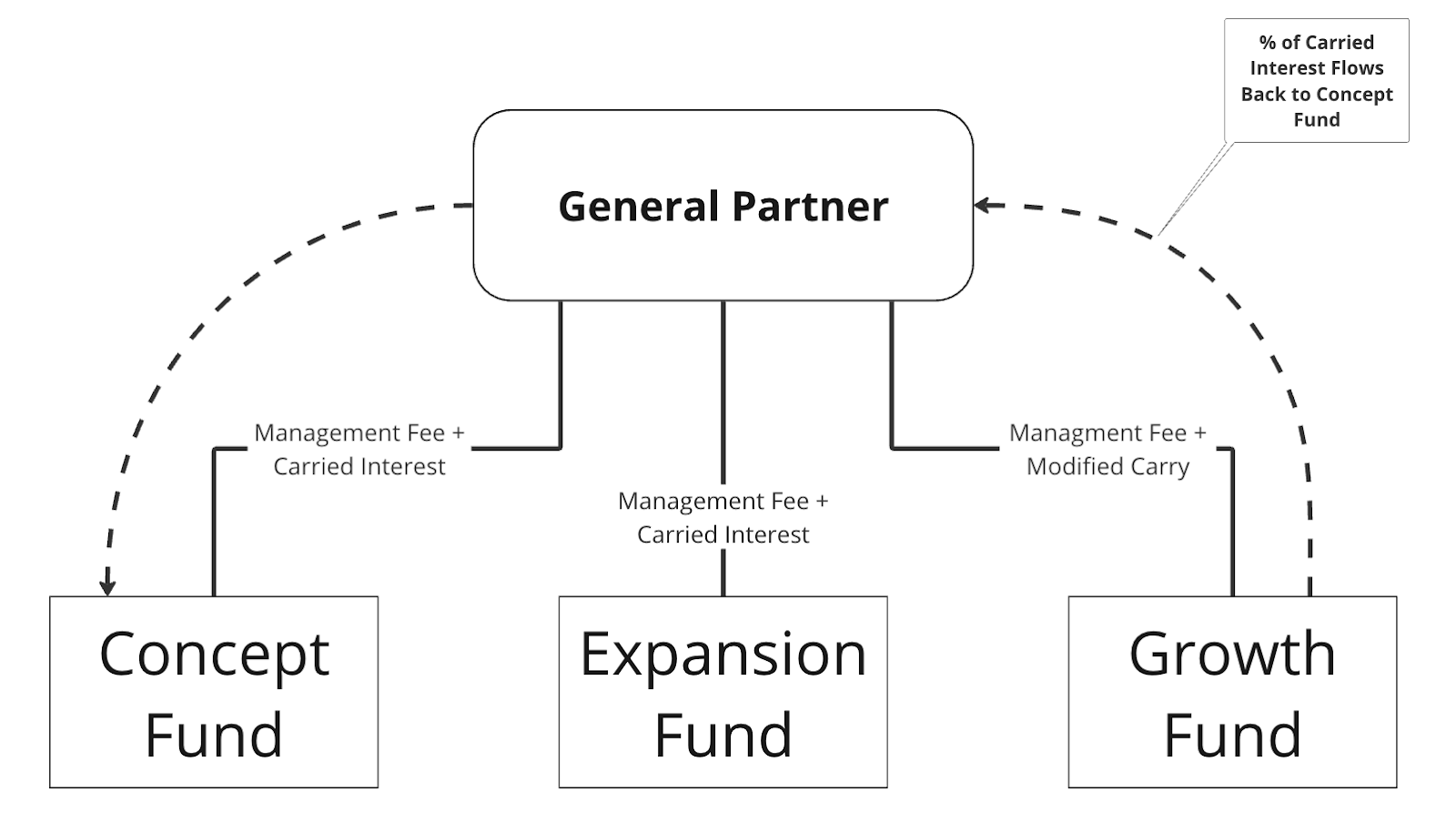

OSS has established its sidecar fund using a classic GP:LP partnership model. They smartly began with a fund that invests in concept-stage ideas, typical of the prevailing venture studio models. To underwrite success, they then set up a fund to invest in the progressive expansion of those startups under development.

Again, a very logical step.

However, their most recent fund added a growth element to their investing strategy, which features a pure-play Evergreen strategy. Rather than raking 100% of the profit derived from the carried interest, OSS is explicitly recycling a significant portion of the returns to perpetuate the venture-building lifecycle.

OSS Ventures is helping to shape its niche focus on the future of manufacturing and industrial operations by providing continuous support and aligning long-term interests as a core investment thesis.

By combining the Evergreen fund structure elements with a venture studio approach, we are looking at a critical building block for the future of the venture investing asset class.

It’s Time for an Industry Wide Strategy Session

As we stand at the precipice of the next wave of technological innovation, it is clear that we must explore new and innovative financing models that align with the long-term growth trajectories of today’s most promising technologies. Evergreen funds, paired with the venture studio model, offer a sustainable and resilient alternative, providing continuous investment and strategic support to startups.

The industry is staring straight into the abyss of the bubble to end all bubbles. We need to embrace the idea of fostering an environment where groundbreaking ideas flourish and mature organically, becoming the new center of gravity for venture investing.

Let’s open up the dialogue on how best to finance the future of innovation so we can ensure that the next generation of startups has the resources and support they need to drive transformative change.